43% of funded startups fail due to poor product-market fit. Validate your banking app idea across four dimensions: market demand, competition, regulation, and features before writing a single line of code.

Skipping validation is the leading reason fintech startups fail. This guide walks through every step to validate a banking app idea: market sizing, competitor mapping, regulatory research, and feature prioritization, so you build on evidence, not assumptions.

Quick Takeaways

-

43% of VC-backed startup failures cite poor product-market fit as the root cause, not running out of money

-

The validation process has six steps: smoke test, market sizing, competitor mapping, regulatory research, feature prioritization, and build decision

-

Regulatory research is non-negotiable before any banking app development. Charter, MTLs, KYC/AML, and data privacy each carry distinct timelines and costs

-

A concierge MVP tests willingness to pay before a single line of code is written

-

Rocket's Solve feature runs the full validation cycle in one structured output: market sizing, competitor mapping, regulatory research, and feature prioritization

Why Do Most Fintech App Ideas Fail Before Launch?

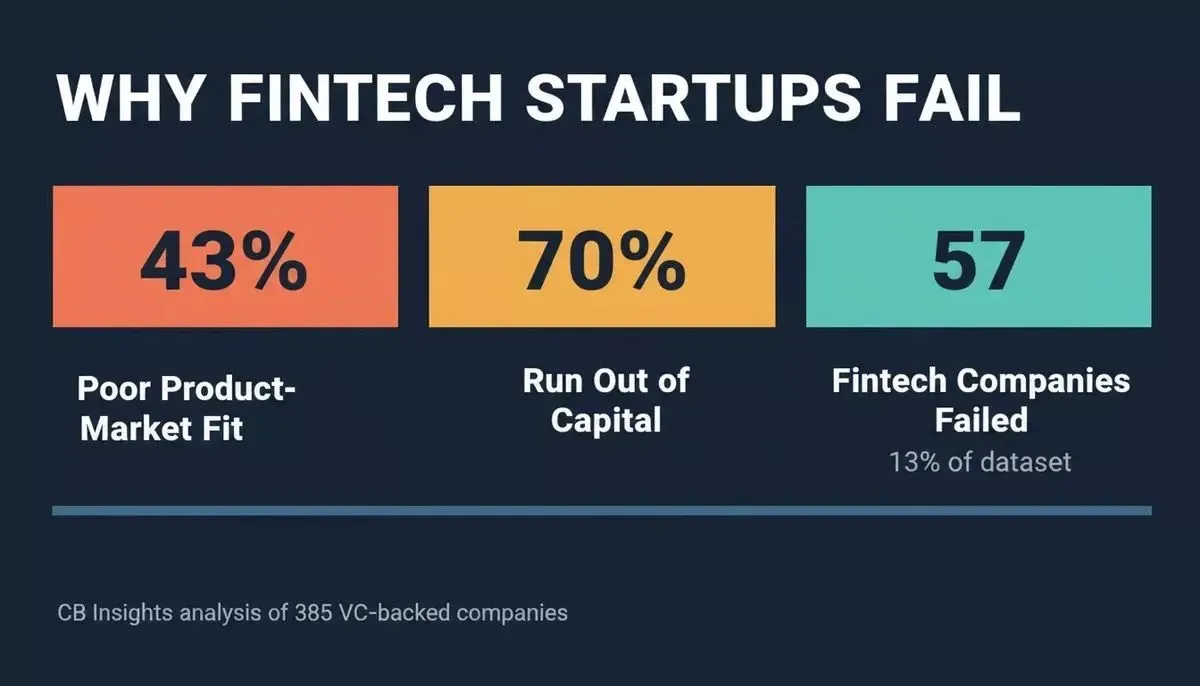

43% of VC-backed startup failures cite poor product-market fit as a primary cause, according to CB Insights research on startup failure. That number gets worse in fintech, where regulatory complexity and development costs make a wrong bet particularly expensive.

Fintech sits in a uniquely dangerous spot for startups that skip validation. The development costs are high, the regulatory path is long, and users hate switching financial services providers unless the pain point is extreme.

-

Product market fit failure dominates the list. Among 385 failed VC-backed companies analyzed by CB Insights since 2023, the core problem was not running out of money. Running out of capital (70%) was the final cause of death, not the root problem. Poor product market fit (43%) and bad timing (29%) reveal why the capital dried up.

-

Fintech ranks second in startup failures by count. 57 fintech companies (13% of the dataset) failed, with a median equity funding of just $4M. Most were early-stage companies in emerging markets that raised during the 2021-2022 boom and struggled with unit economics as capital dried up.

-

Confirmation bias kills good founders. When you fall in love with your mobile app idea, you start looking for evidence that supports it rather than testing whether real users actually need it. This is the single line between founders who ship a successful product and those who spend months building something irrelevant.

Fintech startup failure data: product-market fit failure (43%) and bad timing (29%) are root causes, not capital depletion

The truth is, most fintech founders skip the hard questions. They assume the market exists, guess at what features people want, and start writing code. Six months later, they launch into silence. The fix is not better app development. The fix is better thinking before app development begins, and that thinking has a name: idea validation.

What Does App Idea Validation Actually Mean?

App idea validation is the process of testing whether real people have a painful enough problem to pay for your proposed solution. It is not asking friends if they think your app concept sounds cool. It is structured research that produces a go, pivot, or stop decision before a dollar is spent on development.

The validation process for a banking app covers four dimensions: market interest, competition, regulatory feasibility, and feature prioritization. Understanding how AI-powered research accelerates startup validation can cut this process from weeks to days.

The four dimensions every banking app founder must validate before committing to development

-

Smoke tests tell you if demand exists. A simple page describing your banking app concept, with a waitlist sign-up form, shows whether potential users care enough to act. If nobody signs up, the full app is not worth building.

-

User research separates real problems from assumed ones. Talk to 15-20 people in your target audience. Ask them how they currently handle the problem your app concept addresses. Listen for patterns, not individual opinions.

-

A concierge MVP tests willingness to pay. Before building any code, deliver the core value of your app manually to early users. If people pay for a manual version of your banking service, they will pay for the automated version too.

The goal of this entire process is a clear decision: build, pivot, or stop. Each step gives you data that makes that decision less risky.

The Six-Step Validation Process

Here is the complete validation sequence for a banking app idea, in order:

-

Smoke test: build a page, measure sign-up rate against a 10% threshold

-

Market sizing: calculate TAM, SAM, and SOM using search data and app store signals

-

Competitor mapping: map existing players, read negative reviews, identify gaps

-

Regulatory research: chart the charter/partner bank decision, MTL requirements, KYC/AML, and data privacy obligations

-

Feature prioritization: define must-have vs nice-to-have vs future for your specific MVP

-

Build decision: go, pivot, or stop based on evidence from steps 1-5

The six-step banking app idea validation workflow: each step produces evidence that feeds the next

How Can You Size the Market for a Digital Banking Concept?

Market sizing for a banking app starts with three data sources: search trend trajectory, app store performance data for existing competitors, and industry growth projections. Together, these tell you whether the demand signal is real before you spend anything on development.

-

Google Trends shows the search demand trajectory. Type relevant keywords like "digital savings account" or "fee-free banking app" and check whether interest is growing, stable, or declining over the past 24 months. Growing search volume is a positive sign of market interest.

-

App Store data reveals competitor performance. Tools like Sensor Tower and App Annie (now data.ai) show download volumes, ratings, and revenue estimates for similar apps. If existing banking apps in your niche are pulling millions of downloads, the market is real.

-

The Neobank market is growing fast. According to Plaid's research on neobanks, the industry is expected to grow at a compound annual growth rate of 54.8% between 2023 and 2030. That growth creates room for new entrants targeting specific pain points that existing players ignore.

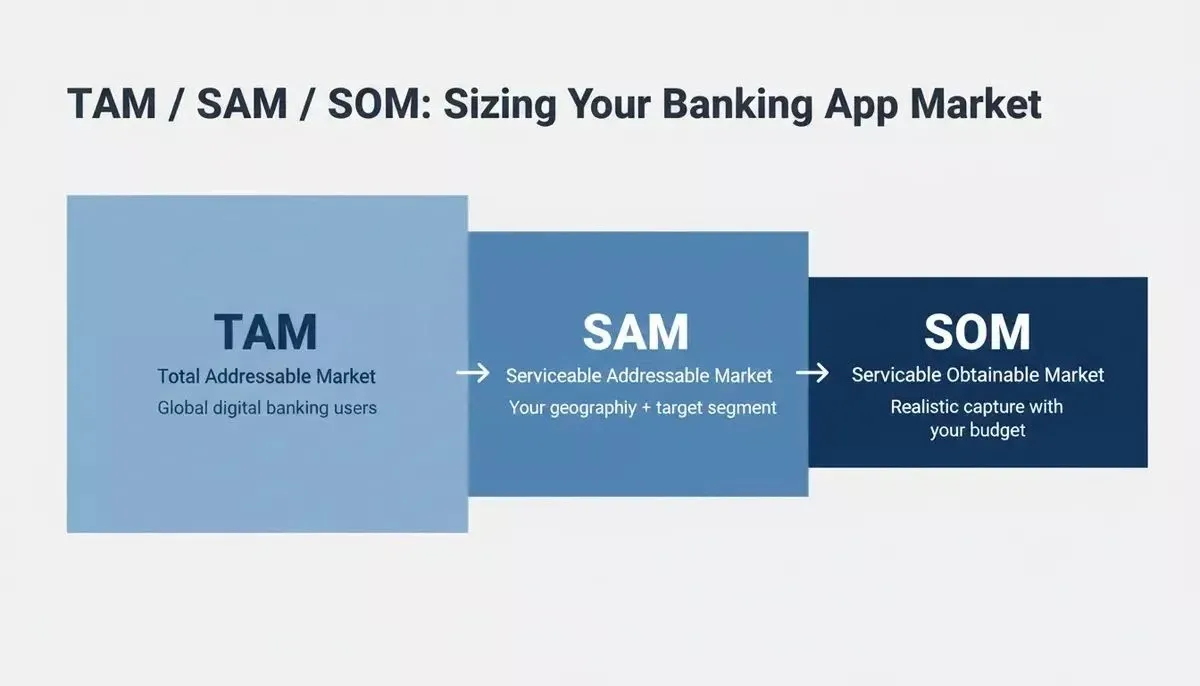

TAM/SAM/SOM applied to a digital banking concept: total addressable market narrows to your geography, audience, and differentiation

Use the TAM/SAM/SOM framework to size your specific opportunity. Your total addressable market is the full global opportunity. Your serviceable addressable market narrows to your geography and target audience. Your serviceable obtainable market is what you can realistically capture with your specific differentiation and budget.

This flow shows how market research connects directly to a build decision. You start broad, narrow through testing, and arrive at a go or no-go signal based on real user behavior, not assumptions. For a deeper look at how to calculate TAM for your specific segment, the TAM/SAM/SOM calculator guide for builders walks through the exact methodology.

Who Are Your Competitors and What Gaps Can You Fill?

Competitor analysis for a banking app starts with mapping existing players by category, then reading negative reviews to find the gaps no one has solved. A crowded market is a good signal: it confirms people pay for solutions in this space. The question is whether you can find a gap worth filling.

-

Map existing players by category. Look at neobanks (Chime, Revolut, Varo), traditional banking apps, and fintech services targeting your specific niche. Check their app store reviews, pricing pages, and feature lists.

-

Read negative reviews to spot pain points. What users hate about existing solutions is your biggest opportunity. If thousands of people complain about the same problem, and no competitor has fixed it, you have a validated gap.

-

Check hiring patterns for strategic direction. If a competitor is hiring compliance engineers and data scientists, they are likely moving into new regulatory territories or adding lending products. Job postings are a leading signal of product direction.

| Competitor Analysis Dimension | What to Check | Where to Find It |

|---|---|---|

| Feature gaps | Missing functionality users request | App Store reviews, Reddit, forums |

| Pricing weakness | Segments underserved by current pricing | Competitor pricing pages, app store listings |

| User complaints | Recurring frustration patterns | Google Play reviews, Twitter/X, communities |

| Geography gaps | Regions without strong local options | App Store availability by country |

| Target audience blind spots | Demographics ignored by incumbents | User research, surveys, early access signups |

| Strategic direction signals | Where competitors are investing next | Job postings, press releases, and funding announcements |

One-time competitor mapping tells you where the gaps are today. Ongoing competitor monitoring tells you when those gaps close or when a new one opens. Rocket's Intelligence pillar watches competitors continuously across four monitoring categories: website changes, social and news activity, customer reviews, and advertising signals.

It delivers daily briefs with structured Intel cards framed to your role and strategic questions, so you do not have to go looking. See how competitive intelligence shapes product decisions on Rocket.

What Regulatory Requirements Should You Check First?

Before spending a dollar on banking app development, map the regulatory path: charter vs. partner bank, money transmission licenses, KYC/AML obligations, and data privacy requirements. Development costs for a fintech app can range from $200,000 to over $1M, and much of that cost comes from compliance, not features.

-

Banking charter vs. partner bank decision comes first. You can either apply for your own banking charter (which takes years and costs millions) or partner with a chartered bank that handles the regulatory infrastructure while you handle the customer experience. Most startups fail when they underestimate this step.

-

Money transmission licenses vary by state. In the US, you may need separate licenses in each state where you operate. Each state has different requirements, timelines, and fees. The Conference of State Bank Supervisors (CSBS) maintains a state-by-state licensing resource for money services businesses.

-

KYC and AML compliance is non-negotiable. Every banking app must verify customer identity and monitor for suspicious activity per FinCEN requirements. This affects your onboarding flow, your development timeline, and your operating costs from day one.

-

Data privacy adds another layer. The Gramm-Leach-Bliley Act (GLBA) governs how financial services handle customer data. Add CCPA compliance for California users and potentially GDPR if you serve European customers.

Banking app regulatory checklist: charter decision, MTLs, KYC/AML, and data privacy each carry distinct timelines and cost implications

The good news: you do not need to solve all of these before testing your app concept. You need to know what the path looks like, what it costs, and whether your business model can support those costs. That is the difference between a validated idea and a naive one. Building a digital wallet or banking experience becomes far less risky once you map the regulatory requirements early.

How Do You Prioritize Core Features for Your Banking MVP?

Feature prioritization for a banking MVP starts with one question: what is the single thing your first users need to experience the core value? Everything else is a future release.

-

Your MVP needs exactly the features that solve your core problem. If your app targets people who hate paying overdraft fees, your MVP needs fee-free accounts and overdraft protection. Nothing else matters on day one.

-

Cut everything that does not directly serve your first users. Budgeting tools, investment accounts, credit score monitoring: these are all nice to have. But if your core value proposition is faster international transfers for freelance designers, ship that and only that.

-

Test willingness to pay before building advanced features. Run simple page tests or pre-order campaigns for each proposed feature. If potential users do not express strong interest in a feature, drop it from your early version.

Group features into must-have, nice-to-have, and future. The must-have list for a fintech MVP is usually shorter than founders think: account opening, money movement, user feedback loops, and basic security. Everything else can wait until you have real users giving you data. For a structured approach to this process, the MVP feature prioritization guide for non-technical founders covers the exact frameworks used by product teams.

Why Rocket Solves Before It Builds

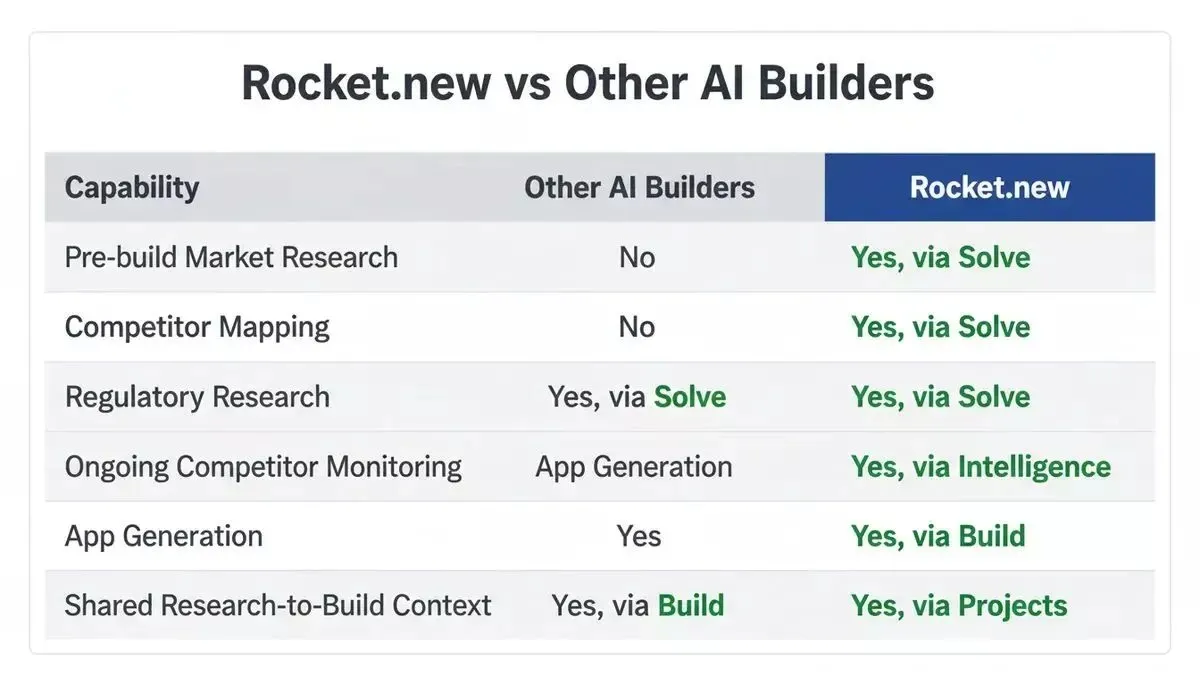

Most AI tools in the market start at the build step. Rocket.new works differently: it validates before it builds. Other platforms like Bolt, Lovable, and v0 start from a blank prompt. They build what you tell them to build. They cannot tell you whether the thing is worth building in the first place. That gap between idea and execution is where most fintech startups fail, and it is the gap Rocket was designed to close.

Rocket.new vs other AI builders: only Rocket combines pre-built research, app generation, and continuous competitor monitoring in one platform

Here is how the Solve, Build, and Intelligence workflow maps to the validation steps in this guide:

-

Solve takes your banking app question and delivers a structured research output. Describe your fintech concept in plain language: "Is there room for a mobile banking app targeting gig workers who struggle with inconsistent income?" Rocket identifies every dimension of the problem, then runs thousands of queries across 150+ sources simultaneously. The output typically covers 8-12 sections, with each finding tagged by signal strength (HIGH, MEDIUM, or LOW) and conflicting signals called out explicitly rather than smoothed over.

-

Within 60 to 90 minutes, you get market sizing, competitor mapping, regulatory research, and feature prioritization in one structured deliverable. You can export the report as a PDF or PPTX presentation to share with co-founders, investors, or advisors.

-

The research output feeds directly into the Build phase. When you decide to build your banking app, the Solve output stays connected inside your Rocket project. Your competitive brief informs the copy. Your regulatory findings shape the onboarding flow. Nothing is lost between research and development: the context carries forward automatically.

-

After launch, Intelligence monitors competitors continuously. Rocket's Intelligence pillar watches every public platform a competitor operates on and delivers structured Intel cards framed to your role and strategic questions. Pricing changes, product launches, hiring signals, and advertising shifts surface automatically.

"I've watched beginners spend 5 to 8 months building a SaaS product before talking to a single customer. No market validation, no paying users, just months of tweaking features in isolation... The hard part is finding out if anyone actually wants what you're building. And that takes one conversation, not six months of building." - Henryk Brzozowski (LinkedIn)

1.5 million people have tried Rocket across 180 countries, from solopreneurs to enterprise teams. For banking app founders specifically, the Solve feature handles the exact steps this guide describes: market sizing, competitor mapping, regulatory research, and feature prioritization, all in one structured output, ready to act on, present, or build from.

The research does not disappear after export: it becomes the foundation of everything that follows in the project. See how Rocket takes you from market validation to a deployed product.

Your Banking App Deserves a Foundation, Not a Guess

The fintech founders who succeed are not the ones with the most brilliant app idea. They are the ones who find out fastest whether people actually need what they are thinking about building, and then build with evidence behind every product decision.

Skip the guessing. Run market research, map your competitors, check the regulatory path, and prioritize features based on real user behavior, not your own assumptions. The entire validation process can happen in days, not months, when you use the right tools.

Ready to validate your fintech concept before writing a single line of code? Describe your banking app idea in plain language on Rocket and let Solve run the research. You will have a structured, evidence-backed decision ready to act on, present, or build from.

Table of contents

- -Quick Takeaways

- -Why Do Most Fintech App Ideas Fail Before Launch?

- -What Does App Idea Validation Actually Mean?

- -The Six-Step Validation Process

- -How Can You Size the Market for a Digital Banking Concept?

- -Who Are Your Competitors and What Gaps Can You Fill?

- -What Regulatory Requirements Should You Check First?

- -How Do You Prioritize Core Features for Your Banking MVP?

- -Why Rocket Solves Before It Builds

- -Your Banking App Deserves a Foundation, Not a Guess